While the private sector lender offered no official reason, the move is widely seen as a bid to extract more value per customer amid pressure on margins.

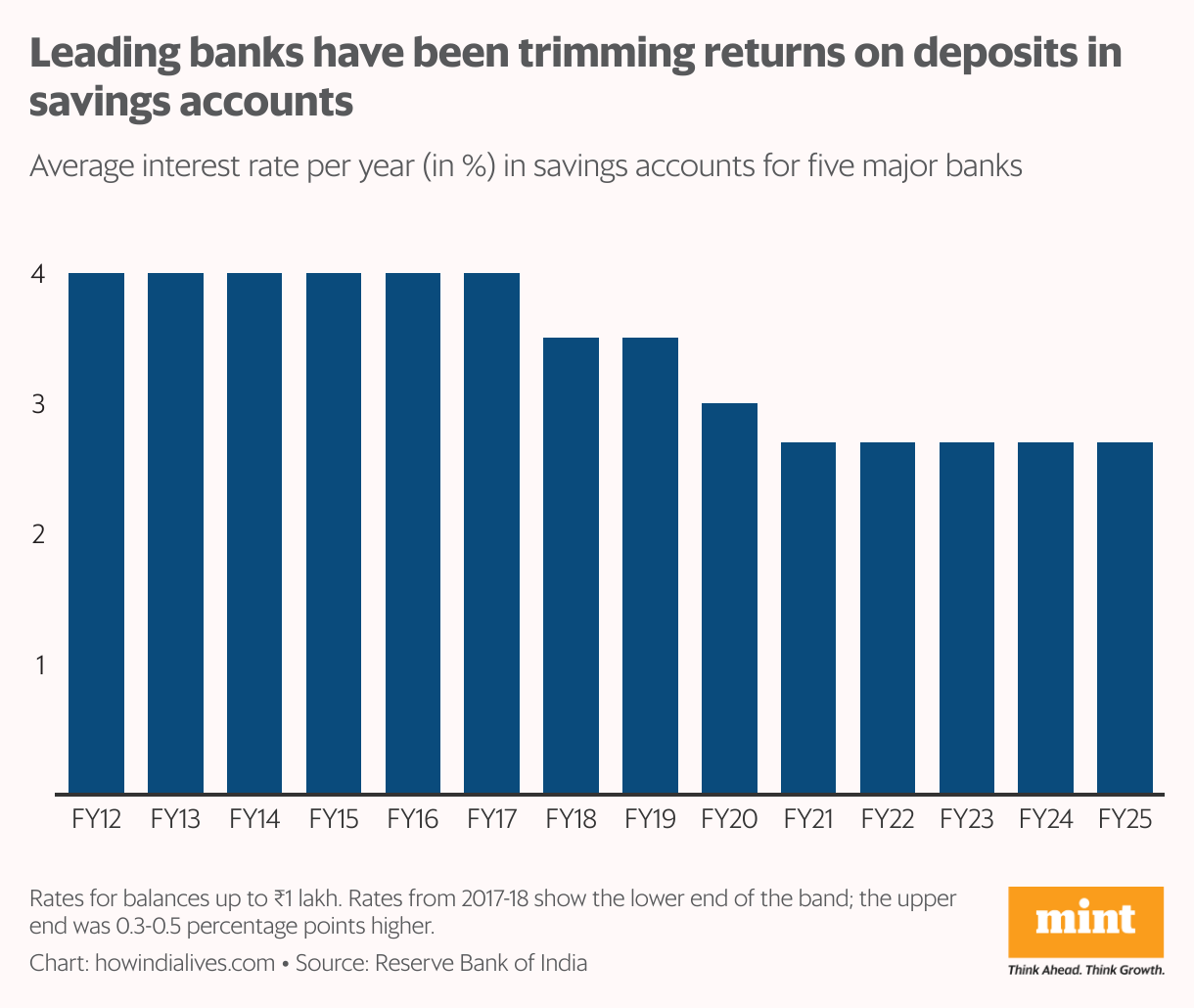

A bank’s core business is straightforward: it collects deposits through current accounts, savings accounts and term deposits, and lends that money at higher interest rates. The gap between what it earns and what it pays—its margin—is a key profit driver. Current accounts, which pay no interest, and savings accounts, which pay nominal rates, are the cheapest sources of funds. The larger a bank’s current account and savings account (Casa) share in total deposits, the lower its cost of funds.

In the past six years, leading banks have seen their Casa figures slide. Since 2011, when the banking regulator allowed savings account rates to be market-determined, large banks have steadily trimmed them. ICICI Bank currently offers 2.5% on savings accounts, and in 2024-25, it paid an average 2.23% interest on Casa deposits. If new customers keep coming in, a higher minimum balance could boost its Casa ratio.

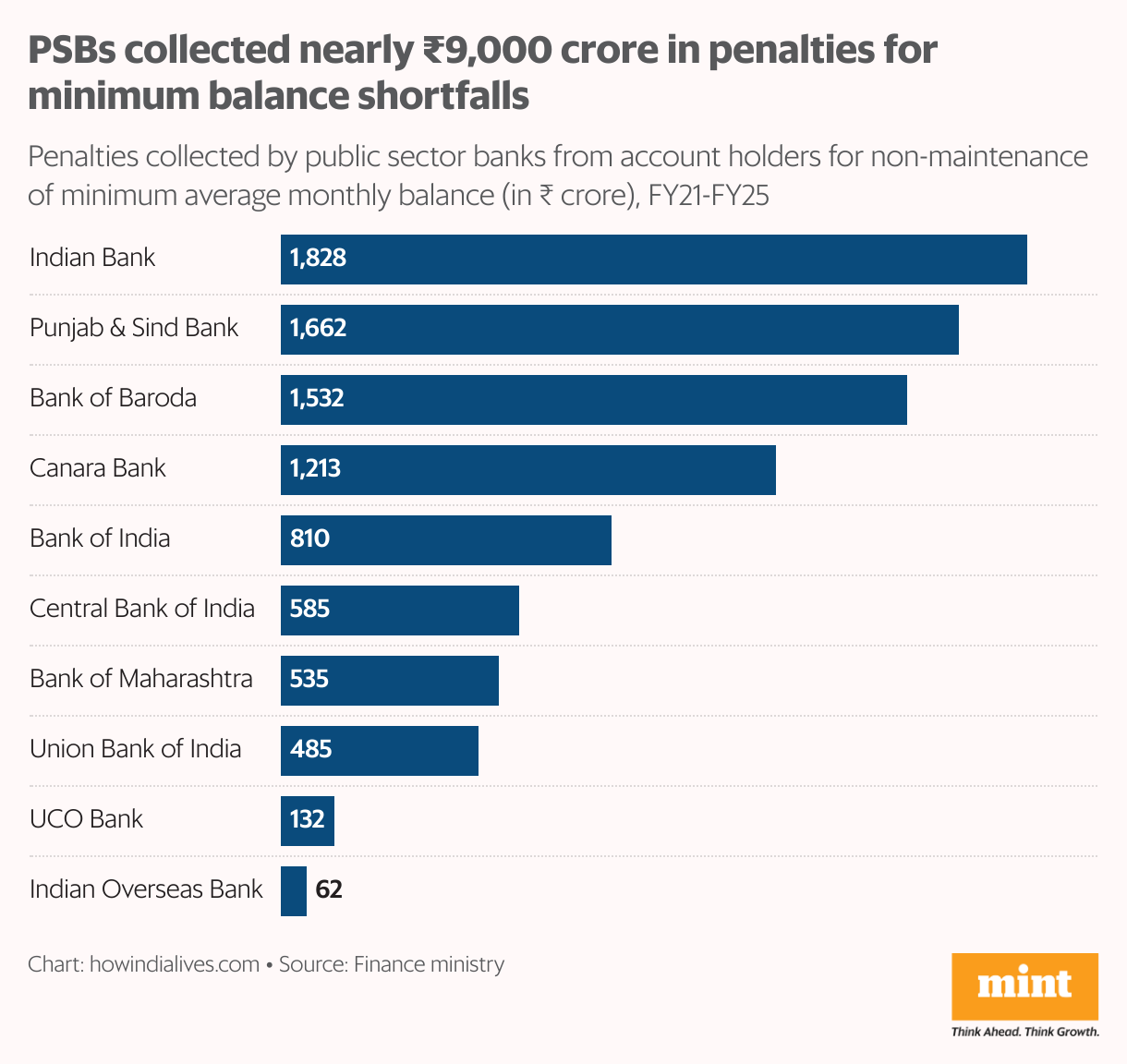

Punitive penalties

However, given that ICICI Bank’s higher minimum balance is only on new accounts, at least for the time being, its effect will be incremental in nature. Even so, it signals a strategic shift towards prioritising quality customers along with growth.

It is a stance that has invited critique. Without naming ICICI Bank, Jay Kotak, co-head of Kotak Mahindra Bank’s mobile banking app, tweeted that “90% of India makes less than ₹25,000 a month”.

ICICI Bank levies penal charges of 6% of the shortfall in the required minimum average balance, or ₹500, whichever is lower. While it does not disclose how much it has collected from such penalties, numbers are available for public sector banks.

Between 2020-21 and 2024-25, 10 public sector banks collected ₹8,844 crore towards such shortfalls. This excludes State Bank of India, which has not levied such charges since March 2020. A few others have also waived this penalty with effect from July 1.

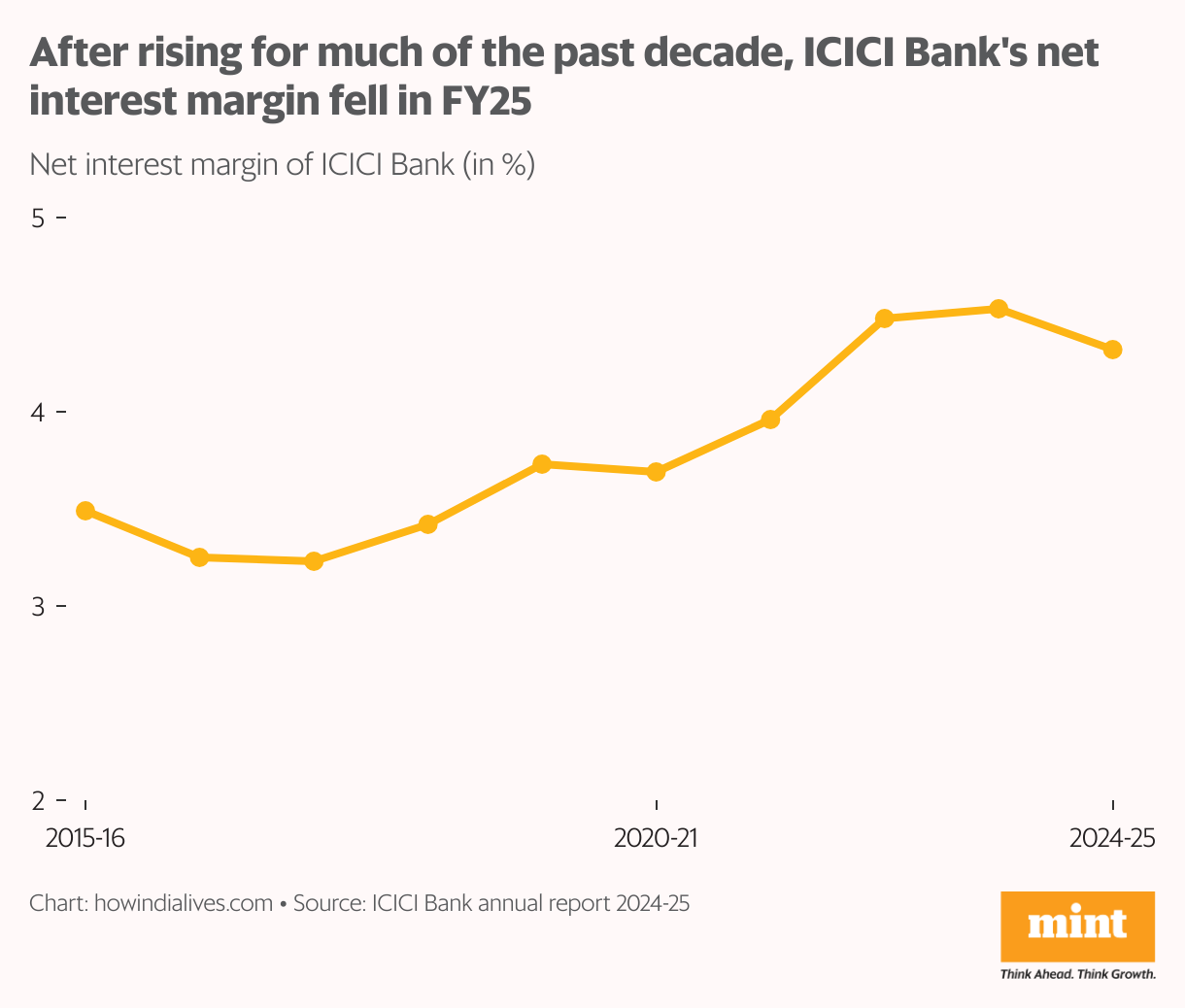

Margin pressure

For ICICI Bank, even a few hundred crores in penalties would be small change. It is India’s third-largest bank by assets and one of the most-reputed across parameters, including customer service. It’s also extremely profitable, in the latest quarter alone, it reported a net profit of ₹12,768 crore.

But under the hood, some key numbers are under pressure.

Between 2023-24 and 2024-25, its cost of deposits increased from 4.61% to 4.91%, with much of the increase in interest coming from what it was paying on term deposits. In 2024-25, its current account and savings account deposits grew at a slower rate than term deposits (13.1% versus 14.6%). As a result, its net interest margin—essentially, its profit margin—fell from 4.53% to 4.32%. In the last eight financial years, going back to 2017-18, this was only the second dip, and a significant one at that.

The pressure on the current account and savings account continues. As of 30 June, ICICI Bank reported a Casa ratio of 41.2%, a further slippage of 0.4 percentage points in three months.

Urban focus

Over the past two decades, ICICI Bank has expanded at a brisk rate, increasing its branch count to 6,903 in March 2025 from 595 in March 2006. In relative terms, the share of metropolitan and urban branches—two of the four geography categories for regulatory purposes—in ICICI Bank’s branch network has dropped from 72% to 51%.

But these two categories of branches account for a larger share of deposits than their branch share. It is these two categories of branches where ICICI Bank was trying to move the needle by raising the minimum balance requirement from ₹10,000 to ₹50,000.

The higher threshold would have given it captive deposits and drawn more high-wallet customers. For now, the lender has settled at ₹15,000—but it’s unlikely to be the last word on the matter, from ICICI Bank or its rivals.

www.howindialives.com is a database and search engine for public data